What is the Asia Pacific Fertilizer Additive Market Overview – definition, scope, and significance?

The Asia Pacific Fertilizer Additive Market encompasses all chemical and functional agents used to improve the performance, handling, and safety of fertilizers across the region. These additives include granular, prilled, and powdered forms, as well as functional categories such as dust control agents, anti‑caking agents, anti‑foam agents, granulation aids, corrosion inhibitors, and hydrophobing agents. They are applied to major fertilizer types—mono ammonium phosphate, triple super phosphate, urea, diammonium phosphate, and ammonium nitrate—to enhance nutrient efficiency, reduce losses, and support sustainable agricultural practices. The market’s significance lies in its role in boosting crop yields, meeting the food security needs of a rapidly growing population, and enabling farmers to adopt precision agriculture while complying with stringent environmental regulations.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Fertilizer Additive Market?

Key drivers include rising demand for high‑productivity agriculture, government initiatives promoting efficient fertilizer use, and increasing adoption of advanced farming technologies. The region’s expanding middle class fuels higher protein consumption, thereby pushing up crop production and fertilizer consumption. Restraints stem from volatile raw material prices and stringent environmental standards that increase compliance costs. Major challenges involve logistics complexities across diverse geographies and the need for farmer education on additive benefits. Opportunities arise from the growing focus on sustainable practices, development of bio‑based additives, and potential for strategic partnerships with agro‑chemical distributors to widen market reach.

What growth trends are currently influencing the Asia Pacific Fertilizer Additive Market?

Current trends include a shift toward granular and powdered additives due to their superior dissolution rates and ease of application. Manufacturers are also investing in multifunctional additives that combine dust control and anti‑caking properties, simplifying formulation for end‑users. Digital agriculture platforms are integrating additive recommendations into precision‑fertilization tools, driving demand for data‑backed solutions. Additionally, there is a noticeable rise in R&D efforts focused on environmentally friendly, low‑toxicity agents that align with the region’s sustainability goals.

How did COVID‑19 impact the Asia Pacific Fertilizer Additive Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains, labor shortages, and reduced purchasing power, which led to a short‑term dip in additive sales. However, the essential nature of food production quickly restored demand, and governments prioritized agricultural inputs to safeguard food security. As restrictions eased, the market rebounded, supported by stimulus packages and a surge in planting cycles. The recovery trajectory remains positive, with a steady return to growth driven by post‑pandemic emphasis on resilient and efficient agricultural inputs.

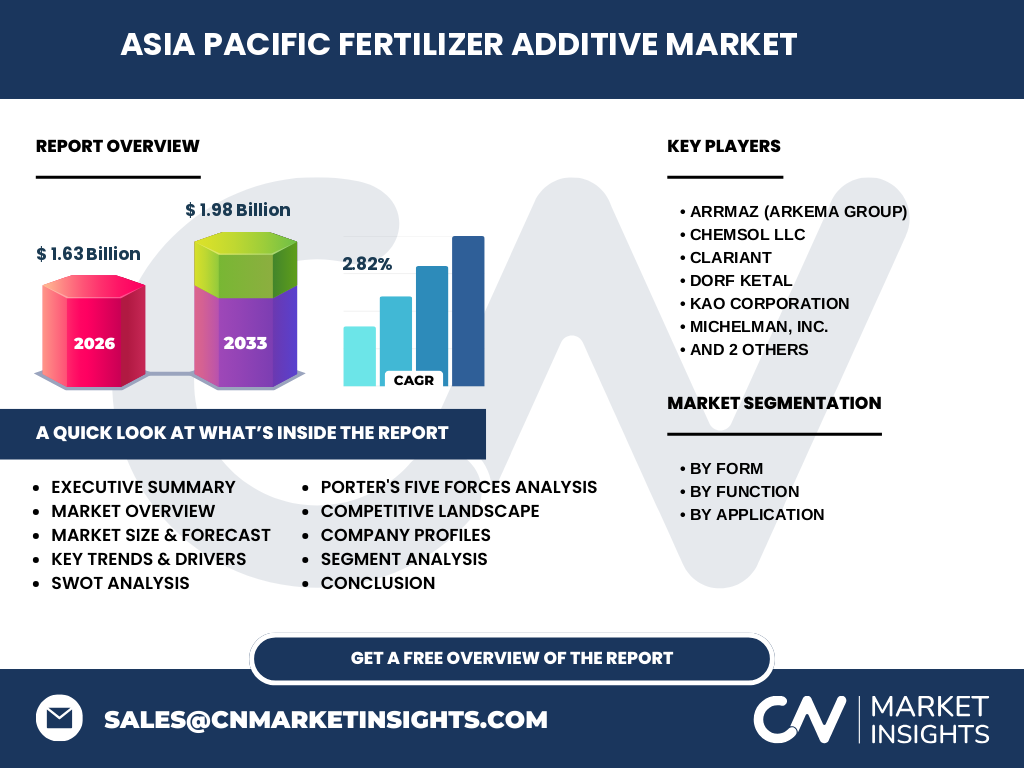

Who are the major competitors and what is the level of consolidation in the Asia Pacific Fertilizer Additive Market?

The competitive landscape is characterized by a mix of global chemical giants and specialized regional players. Leading companies include Arrmaz (Arkema Group), Chemsol LLC, Clariant, Dorf Ketal, KAO CORPORATION, Michelman, Inc., Omex Agriculture, Inc., and Solvay. These firms compete on product innovation, breadth of functional offerings, and strategic distribution networks. Recent years have witnessed a moderate degree of consolidation through mergers, acquisitions, and strategic alliances aimed at expanding product portfolios and strengthening geographic presence, particularly in high‑growth economies such as China, India, and Southeast Asia.

What are the key findings highlighted in the executive summary of the Asia Pacific Fertilizer Additive Market?

The executive summary underscores a market valued at USD 1.63 billion in 2026, with a projected increase to USD 1.98 billion by 2033, reflecting a CAGR of 2.82 % over the forecast horizon. Growth is propelled by rising agricultural demand, regulatory encouragement of efficient fertilizer use, and ongoing innovation in additive technologies. Competitive dynamics are shaped by a handful of well‑established players leveraging R&D and strategic partnerships. The report emphasizes substantial opportunities in sustainable additive development and the integration of digital agriculture solutions.

What are the forecast expectations for the Asia Pacific Fertilizer Additive Market from 2025 to 2032?

Based on the provided CAGR of 2.82 %, the market is expected to maintain a moderate yet steady upward trajectory. By 2032, the market size is anticipated to approach the upper range of the forecast band, reinforcing the sector’s resilience and its alignment with broader agronomic trends. This growth will be underpinned by continued expansion of the fertilizer base, increased adoption of high‑efficiency additives, and ongoing regulatory support for environmentally responsible farming practices.

How is the Asia Pacific Fertilizer Additive Market sized and shared across its segmentation?

Segmentation by form divides the market into granular, prilled, and powdered additives, each catering to specific application methods and handling requirements. Functional segmentation includes dust control agents, anti‑caking agents, anti‑foam agents, granulation aids, corrosion inhibitors, and hydrophobing agents, reflecting the diverse performance enhancements sought by fertilizer manufacturers. Application segmentation covers major fertilizer types—mono ammonium phosphate, triple super phosphate, urea, diammonium phosphate, and ammonium nitrate—illustrating the broad relevance of additives across the fertilizer spectrum. While precise share values are not disclosed, the granulated and powdered forms, together with dust control and anti‑caking functions, represent the core volume drivers.

What is the geographic distribution of the global Asia Pacific Fertilizer Additive Market?

The market’s geographic footprint spans the entire Asia Pacific region, with significant activity concentrated in East Asia (China, Japan, South Korea), South Asia (India, Bangladesh), and Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia). These sub‑regions collectively account for the majority of market demand due to their extensive arable land, intensive cropping systems, and proactive agricultural policies. The strong manufacturing bases in China and India further reinforce regional dominance in both production and consumption of fertilizer additives.

What does the regional analysis reveal about market performance within the Asia Pacific Fertilizer Additive Market?

China remains the largest contributor, driven by its massive fertilizer consumption and ongoing reforms to improve nutrient use efficiency. India follows closely, propelled by government schemes encouraging balanced fertilization and the adoption of modern inputs. Southeast Asian economies exhibit rapid growth, fueled by rising per‑capita incomes, expanding cultivated areas, and increased investment in agritech. Each sub‑region demonstrates unique growth catalysts, yet all benefit from the overarching trend toward higher‑value, performance‑enhancing additive solutions.

Which companies lead the Asia Pacific Fertilizer Additive Market and what are their strategic approaches?

Arrmaz (Arkema Group) leverages its broad chemical expertise to offer customized additive blends. Chemsol LLC focuses on niche functional agents with strong anti‑caking performance. Clariant emphasizes sustainable chemistry, developing bio‑based additives. Dorf Ketal invests heavily in R&D to introduce next‑generation granulation aids. KAO CORPORATION utilizes its extensive distribution network across Japan and South Korea. Michelman, Inc. pursues strategic acquisitions to expand its product portfolio. Omex Agriculture, Inc. concentrates on collaboration with regional fertilizer producers, while Solvay integrates its global innovation pipeline to address local market needs.

How does Porter’s Five Forces framework assess the competitive environment of the Asia Pacific Fertilizer Additive Market?

Threat of new entrants is moderate; high capital requirements and stringent regulatory compliance deter newcomers. Bargaining power of suppliers is relatively low, as raw material sources are diversified globally. Bargaining power of buyers—large fertilizer manufacturers—remains significant, prompting additive suppliers to differentiate through performance and sustainability. Threat of substitutes is limited, given the specialized function of additives. Industry rivalry is intense, driven by product innovation, pricing strategies, and strategic alliances among established players.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Asia Pacific Fertilizer Additive Market?

Strengths: Robust demand driven by agricultural growth, established expertise of key players, and a wide array of functional products. Weaknesses: Sensitivity to raw material price fluctuations and the need for continuous technical support to end‑users. Opportunities: Development of eco‑friendly additives, expansion into emerging markets, and integration with digital farming platforms. Threats: Regulatory changes imposing stricter emission standards, potential supply chain disruptions, and competitive pressure from low‑cost alternative chemicals.

How is value created and transferred along the Asia Pacific Fertilizer Additive value chain?

The value chain begins with raw material sourcing (e.g., specialty chemicals, polymers), followed by formulation and manufacturing of additive blends. Subsequent stages include quality testing, packaging, and distribution through specialized chemical distributors or direct partnerships with fertilizer manufacturers. End‑users—fertilizer producers—integrate additives during granulation or blending processes, ultimately delivering enhanced fertilizer products to growers. Value is added at each step through innovation, regulatory compliance, and logistical efficiency.

What investment insights can be drawn for stakeholders interested in the Asia Pacific Fertilizer Additive Market?

Investors should focus on companies with strong R&D pipelines targeting sustainable and multifunctional additives, as these are likely to capture premium market segments. Strategic investments in joint ventures with regional fertilizer producers can accelerate market entry and distribution. Additionally, funding digital platforms that provide additive recommendation engines presents a high‑growth avenue, aligning with precision agriculture trends. Monitoring regulatory developments will help mitigate compliance‑related risks.

What are the key conclusions and takeaways from the Asia Pacific Fertilizer Additive Market analysis?

The market is poised for steady growth, underpinned by a solid base of agricultural demand and supportive policy environments. Competitive dynamics favor firms that combine technological innovation with strong distribution networks. Sustainable and digital enhancements represent the next frontier for differentiation. Overall, the sector offers attractive long‑term prospects for stakeholders who can navigate raw material volatility and regulatory complexities.

What research methodology was employed to compile this market report?

The study utilized a mixed‑method approach, combining primary interviews with industry experts, surveys of fertilizer manufacturers, and secondary data collection from reputable industry publications, government statistics, and company annual reports. Quantitative analysis involved trend extrapolation based on the provided market size (USD 1.63 billion in 2026) and forecast (USD 1.98 billion for 2027‑2033) using the stated CAGR of 2.82 %. Qualitative insights were derived from expert opinion and competitive benchmarking.

What is the scope of this research and its limitations?

The research covers the full spectrum of fertilizer additives used in the Asia Pacific region, segmented by form, function, and application. Geographic scope includes major sub‑regions such as East, South, and Southeast Asia. Limitations arise from the reliance on publicly available data and disclosed company information; proprietary sales figures and detailed market shares are not disclosed. Nonetheless, the analysis provides a comprehensive view of market dynamics and strategic directions.

Which key companies are highlighted and what recent developments have they announced?

Arrmaz (Arkema Group) recently launched a low‑phosphorus dust control agent tailored for urea fertilizers. Chemsol LLC introduced a new anti‑caking polymer that enhances storage stability under high humidity. Clariant announced a partnership with a leading Indian fertilizer producer to co‑develop bio‑based anti‑foam additives. Dorf Ketal reported the acquisition of a niche granulation aid startup, expanding its product portfolio. KAO CORPORATION unveiled an advanced corrosion inhibitor for ammonium nitrate blends. Michelman, Inc. completed a strategic alliance with a Southeast Asian distributor to broaden market reach. Omex Agriculture, Inc. rolled out a digital advisory platform integrating additive usage recommendations. Solvay invested in a joint R&D facility focused on hydrophobing agents for triple super phosphate.